On Bitcoin ETF Options

The Coming Explosion in Volatility of Volatility

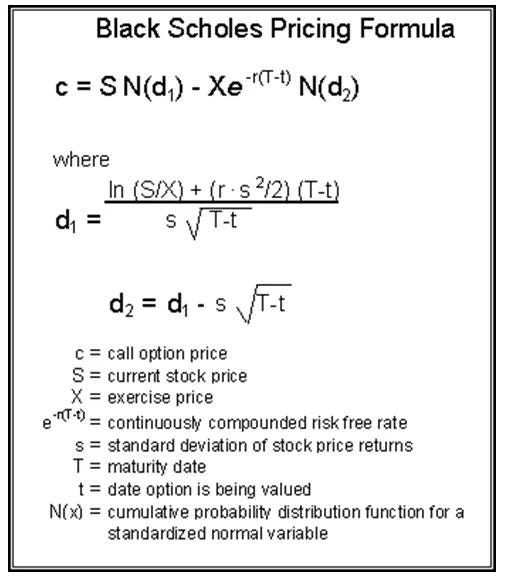

All models have faults - that doesn't mean you can't use them as tools for making decisions. - Myron Scholes

With today’s historic approval by the SEC to list and trade Bitcoin ETF options, we stand on the verge of witnessing what could become the most extraordinary upside in vol of vol (volatility of volatility) in financial history. To fully appreciate…